Why Rewards Timing Matters - ProductFTW #71

A few weeks ago, we wrote about payment timing and why it is a product decision, not just an operational one. That post led to a bunch of side conversations internally about other timing decisions we make without always calling them product choices. The one that keeps coming up for me is rewards.

When you are building a payment product with a rewards component, you spend a lot of time debating earn rates, bonus categories, partner offers, burn mechanics, and all the fun stuff. We will probably write more about designing a rewards system in later posts, but what I want to focus on here is simpler and more foundational: when rewards are attributed, when they are usable, and why those decisions matter more than people think.

The sequencing of rewards

Before getting into tradeoffs, let’s align on definitions. I think about rewards in three states: earned, available, and redeemed.

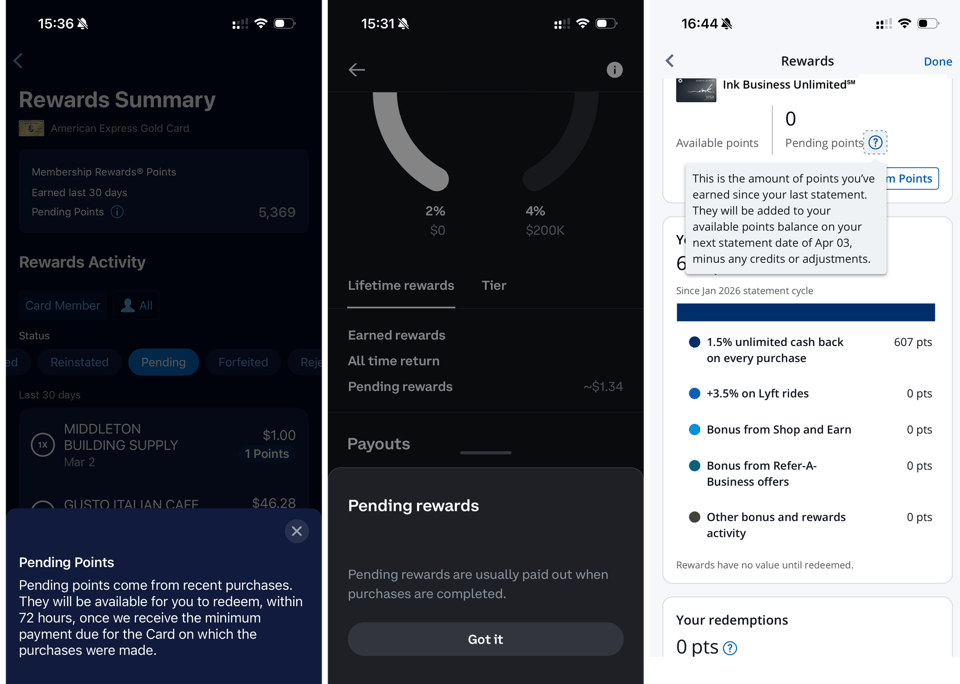

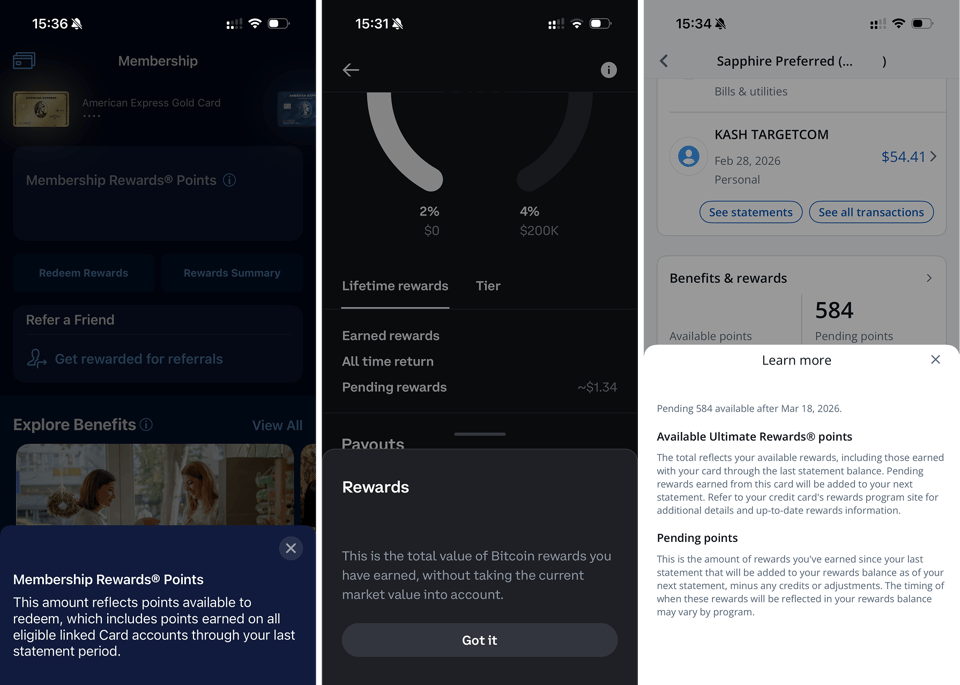

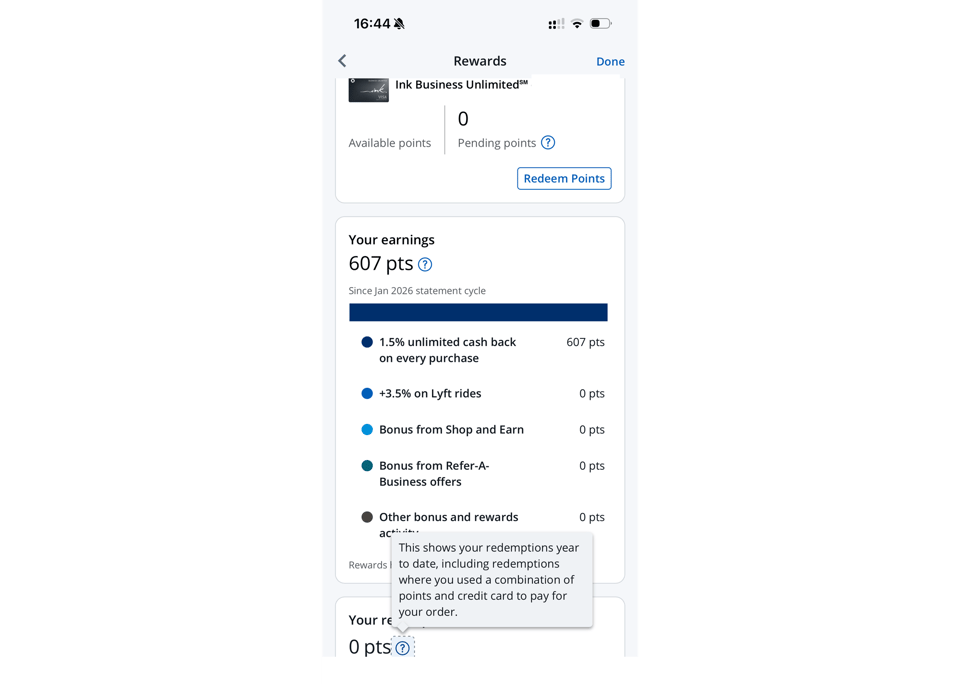

Earned is when you make a transaction that qualifies for a reward, and you are granted points. They show up somewhere in the product. They exist in your balance. They are not yet usable.

Available is when those points can actually be redeemed. This is the moment the user can apply them to a statement credit, convert them to cash, transfer them, or use them in whatever redemption flow you support.

Redeemed is exactly what it sounds like. The points have been used and are no longer available.

These definitions are straightforward. The complexity comes from deciding when each of these states is triggered. Each trigger has a downstream impact on user experience, support load, fraud risk, accounting, and even marketing.

When are points earned?

The first decision is when to mark rewards as earned.

One option is to attribute rewards immediately upon authorization of the transaction. This means the user spends and almost immediately sees how much they earned. Coinbase does this with BTC rewards. The feedback loop is tight and intuitive. I spend, and I see the reward. It reinforces the value proposition in real time.

From a product standpoint, this is a great experience. It feels modern and transparent, and it helps users connect behavior to benefit.

From an operations standpoint, it can be messy. Authorized transactions are not final. Tips get added, amounts can change, and transactions fall off. If you show rewards instantly and the underlying transaction adjusts before settlement, the reward number may need to change. When that happens, users assume something broke. Support ends up explaining settlement mechanics to people who do not care about settlement mechanics.

The more traditional approach is to attribute rewards at settlement. At that point, the transaction amount is final, accounting is cleaner, and you avoid the tip adjustment problem. Your ledger aligns with your processor, and your finance team is happier.

The downside is obvious. The user may wait a few days for the rewards to appear. The reinforcement loop is slower. If you are positioning your product as fast and delightful, this delay can feel out of sync with the rest of the experience.

There is no universally correct answer. The right choice depends on what you are optimizing for and how much operational complexity you are willing to absorb.

When do points become available?

Earning is only the first layer. The second decision is when those earned points become available.

You can make them available immediately upon settlement. You can batch them at the end of the settlement day. You can unlock them at the end of the statement period. Some programs add extra holding periods for specific categories or high-risk transactions.

This decision is really about risk tolerance.

Even settled purchases can be returned. Chargebacks happen. Fraud is sometimes detected days or weeks later. If you make points available immediately and the user redeems them, you may have to claw back value when the underlying transaction reverses. Clawbacks are painful. They create negative balances and confusing experiences. They also generate support tickets from users who feel like something was taken away from them.

If you delay availability until the end of the statement cycle, you significantly reduce that risk. Returns and disputes often surface within that window. You gain time to reconcile before letting value leave the system.

The tradeoff is that users see points sitting in their account that they cannot use yet. If that gap is not clearly explained, it feels arbitrary. Even if it is explained, the program can still feel less flexible.

Some teams try to get more nuanced. They unlock low-risk transactions quickly and hold higher-risk ones longer. Others tie availability to risk scores. That approach can work, though it adds engineering and data complexity that not every team is ready for.

How timing shapes perception

What I find interesting is how much these timing decisions shape perception, even when the earn rate is identical.

If rewards are earned and available instantly, the program feels generous and responsive. The reward feels embedded in the purchase itself.

If rewards are earned at settlement and only available at the end of a billing cycle, the program feels more like a periodic rebate. That model has worked for decades in credit cards. It just sets a different expectation.

Clarity is more important than speed in most cases. If users understand that rewards will show up after settlement and unlock at the end of the statement period, frustration drops. Confusion usually comes from misalignment between what the user expects and what the system actually does.

This is where product design has to do more than legal copy. Terms and conditions are necessary. The UI should clearly distinguish between earned, available, and redeemed. Transaction-level detail should explain why something is not yet usable. State should be visible and intuitive.

When users can see what is happening and why, they are far more forgiving of delays.

The financial and operational side

Rewards are a liability. The moment points are earned, the program is accruing cost. The moment they are redeemed, that cost becomes real. Shifting the timing of earning and availability changes how that liability shows up on your balance sheet.

If you accelerate earning and availability, you accelerate potential redemption. If your economics rely on breakage assumptions, timing changes can materially impact your forecasts.

There is also fraud exposure. Instant availability can be exploited in edge cases, especially with merchant-funded rewards or category bonuses. Tight controls and clawback logic help. They rarely eliminate all risk.

This is why I keep coming back to the idea that timing is a product decision. It touches risk, finance, operations, engineering, and support. It also directly shapes how users perceive the value of your program.

Designing intentionally

The best rewards programs are not necessarily defined by delivering rewards the fastest. They are the most coherent. The timing of earned, available, and redeemed aligns with the brand, the risk appetite, and the operational maturity of the company.

If your product promise is speed and transparency, showing earned rewards instantly may be worth the operational friction. If your margins are thin and your scale is large, tighter controls and delayed availability may be the responsible choice.

What matters is that you choose intentionally. Timing should not be inherited from your processor or copied blindly from a competitor. It should reflect your strategy and your constraints.

About ProductFTW

ProductFTW is a weekly newsletter about product management, with a focus on real-life experiences in startups. We want to help product leaders be successful by giving realistic approaches that aren’t for giant tech companies. We know you don’t have a full-time product designer on each team. We know your software probably hasn’t been used by millions of people worldwide–yet. We’re here to bridge the content gap from building your product and team to scaling it.

Part of the Fintech Product Management Field Guide — ProductFTW's writing on what makes building card, payment, and banking products different.