Credit Card Repayment Timing Is a Product Decision - ProductFTW #68

Have you ever wondered what the last possible moment is to make your credit card payment without it being late?

If you haven’t, that’s great. If you’ve ever been tight on cash, waiting on a paycheck, or just mildly curious, you’ve probably assumed that the answer should be easy to find in your credit card app.

As it turns out, sometimes it isn’t. The exact cutoff time can be buried three or four clicks deep, hidden behind generic “due today” language that sounds clear until it’s 10:47 pm and you’re doing the math in your head.

Not every user can pay early. When you’re tightly managing your money, timing matters. The less clear the product is about that timing, the more anxiety it creates right at the moment someone is trying to do the responsible thing.

In Product FTW #67, I wrote about repayment options and why the boring-looking text on a payment screen matters more than it seems. This week is about timing: when a payment is made, when it’s applied to an account, and when it’s considered “on time.” These are often treated as implementation details, but they shape how users experience repayment each month, especially when they’re trying to avoid late fees.

When a Payment Counts

Most users assume a payment is applied the moment they hit submit. That assumption is reasonable. It just doesn’t align with how many credit products work, which is why repayment generates so many support tickets.

At a high level, issuers tend to make one of two choices.

Some apply a payment immediately when the user submits it. The balance drops, available credit increases, and the product reflects the action right away. American Express is a common example of this approach. Seeing your balance move immediately is oddly satisfying. It doesn’t change how much money you have, but it reassures users that something happened and the payment actually went through.

Other issuers wait until the payment posts and clears before updating the balance and available credit. This approach is more common, especially among smaller issuers and newer programs.

Neither option is “right.” They optimize for different tradeoffs.

Applying payments immediately improves perceived responsiveness, but it introduces risk. The payment can still fail due to insufficient funds, a canceled transfer, or bank issues. In the meantime, the user may already have spent the additional available credit. When that happens, the product has created a problem it now needs to unwind.

Waiting until the payment posts reduces that risk, but it creates a different kind of confusion. From the user’s perspective, they paid their bill, nothing changed, and now they’re wondering whether they misunderstood something or clicked the wrong button. The system is behaving exactly as designed, but the experience doesn’t make that obvious.

“Why Is My Payment Still Pending?”

Timing becomes visible when payments take longer than users expect.

How long a payment takes to apply depends on when it is made, the payment method, the user’s bank, and whether weekends or holidays are involved. In practice, three to five business days is typical, even though it rarely aligns with user expectations.

Even the time of day matters. Payments made late in the evening are often treated differently than those made earlier, because bank cutoff times determine whether a payment is considered same-day or pushed to the next business day. Most users have no idea those cutoff times exist, and there’s no reason they should.

From the system’s point of view, a pending state is normal. From the user’s perspective, their money has disappeared into the void.

If someone makes a payment on Thursday night and a long weekend follows, that payment may still be pending on Tuesday. Nothing is broken, but unless the product sets expectations clearly, the experience feels unreliable.

Most repayment experiences don’t explain what “pending” actually means. Users don’t think in business days or clearing windows. They think in calendar days, and when money is involved, several days without visible movement are enough to create doubt.

If a product waits until payments post before updating balances, that choice needs to be explicit. Showing the time the payment was made, highlighting cutoff times, and setting expectations for multi-day posting help users understand what’s happening rather than assuming they made a mistake.

When is a Payment Considered Late?

Regardless of how payments are applied, users need clarity around one thing in particular: when the late window actually begins.

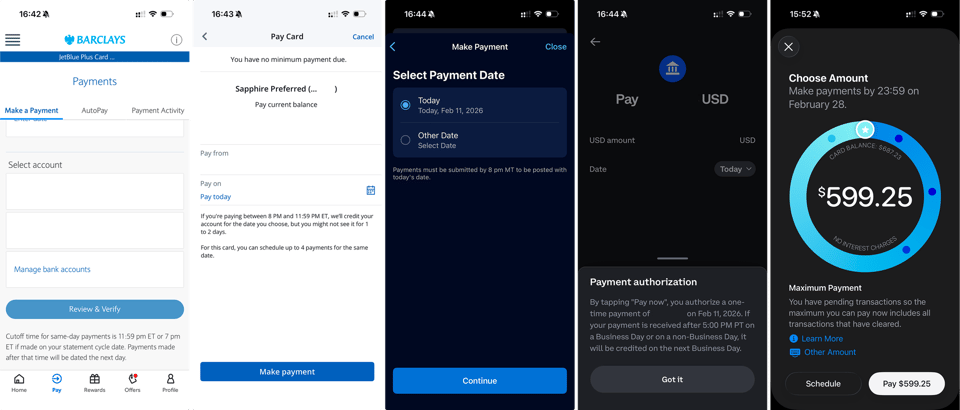

Most credit card products allow payments up to a specific cutoff time on the due date, typically around midnight Eastern Time, even on weekends. Whether Eastern time is used because of banking infrastructure or simple convention matters less than whether the product communicates it clearly.

This is where vague language creates unnecessary stress. “Pay by today” sounds fine until it’s late at night and someone is trying to decide whether they still have time. “Pay by 11:59 PM ET” answers that question immediately.

Some products handle this better than others. Apple Card is a good example of using limited screen space to reduce ambiguity by displaying the exact cutoff time rather than relying on date-based phrasing.

The Complexities of Autopay

Autopay exists for many reasons. It reduces missed payments, users like not having to think about due dates every month, and it generally improves on-time payment rates. Implementing it is where things become more complicated because autopay still operates under the same constraints as manual payments: weekends, holidays, bank cutoff times, and posting delays still apply.

When an autopay payment is delayed or fails, the experience is often worse than a missed manual payment. The user followed the product’s recommendation, and the outcome still didn’t match their expectations.

Autopay also creates edge cases with one-time payments. If a user submits a manual payment that is still pending, product teams need to decide whether to run autopay, adjust it, cancel it, or wait. If both payments go through, the user can easily overpay their balance.

Allowing overpayment creates downstream operational work. Once a user pays more than they owe, the issuer now owes the user money. Returning those funds, ensuring delivery, and tracking unresolved balances introduces additional complexity, including unclaimed funds and escheatment obligations if the money is not successfully returned. At that point, you’re no longer just building a repayment flow. You’ve created a very small, very annoying refund operation.

The safest approach is usually to prevent overcollection in the first place. Autopay needs guardrails that account for pending payments so the system never takes more than the user owes.

Conservative Timing Is Usually the Right Choice

Some large issuers can afford to be aggressive with repayment timing because they have the balance sheet, controls, and operational maturity to apply payments early and deal with failures later. Most startups do not.

Waiting for payments to post reduces risk and avoids situations where users spend money that has not actually cleared. That choice doesn’t have to result in a bad experience, as long as the product explains what is happening and sets expectations clearly.

Different products will make different choices. Secured cards, charge cards, and revolving credit all behave differently, and that’s fine. What matters is that these timing decisions are intentional and visible to users.

Where This Actually Shows Up

Repayment timing rarely looks like a feature. It shows up as a timestamp, a cutoff notice, or a small line of text that most users barely notice.

Those details are where expectations are either set correctly or quietly broken. When users understand when a payment counts, pending states feel normal. When they don’t, delays feel suspicious.

If you care about limiting confusion at the moment of repayment, timing deserves far more attention than it usually gets.

About ProductFTW

ProductFTW is a weekly newsletter about product management, with a focus on real-life experiences in startups. We want to help product leaders be successful by giving realistic approaches that aren’t for giant tech companies. We know you don’t have a full-time product designer on each team. We know your software probably hasn’t been used by millions of people worldwide–yet. We’re here to bridge the content gap from building your product and team to scaling it.

Part of the Fintech Product Management Field Guide — ProductFTW's writing on what makes building card, payment, and banking products different.